Australia, why aren’t you cutting interest rates yet?

18 October 2024

Tourist and alternative lifestyle mecca Byron Bay may be getting stripped of its nudist beach but it is the RBA that is getting embarrassed by larger than expected figures! Meanwhile, the EU has started cutting, the US remains on course for cuts, Japan is excited about tightening, and New Zealand exits recession.

What happened in Australia?

The monthly CPI indicator for May surprised the market on the upside for the third month in a row (see chart below) and is now back at 4%. The RBA’s preferred inflation measure, trimmed CPI, has now risen for the fourth month in a row.

Phil O'Donoghue, Chief economist at Deutsche Bank, has called Australia’s inflation “intolerably high” compared to our peers while the local media believe that the RBA has been caught out by not raising rates high enough during the current cycle and may now be forced to raise rates again before they cut them. The RBA Board kept rates steady in June.

The stage three tax cuts in July and the wealth effect from rising real estate prices are not helping the RBA’s fight against inflation.

Michele Bullock’s narrow path to a soft landing is now the width of a bikini string and if the June monthly and quarterly CPI does not show inflation slowing, the RBA may feel more than a little exposed as the local media shark pack increase the intensity of their attacks on the institution, particularly as the number of other central banks cutting rates grow.

If the RBA raises rates at its August Board meeting, a rise it has considered the last two meetings, then the odds of a recession greatly increases. Independent and former ANZ chief economist Saul Eslake believes that the odds of recession will increase from 10% to 50% with another rate rise.

“If inflation doesn’t come down, we have an issue and the Board won’t hesitate to act if it feels that inflation isn’t coming down quickly enough or if inflationary expectations are starting to rise.” Michele Bullock at the Senate House Economics Committee, 5 June 2024.

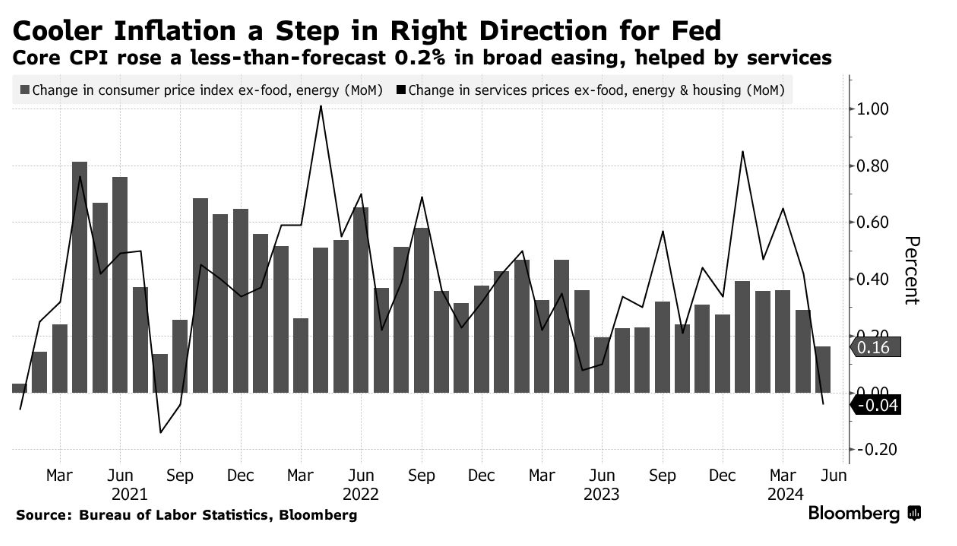

The US is heading towards its first cut.

US CPI was lower than expected for May with no change in monthly inflation and a 0.16% increase in monthly core inflation (see chart below). Services inflation excluding energy, food, and housing actually decreased by 0.04%. Recently rampant car insurance premiums decreased for the first time since 2021.Core inflation increased 3.4% on an annual basis, the lowest pace in over three years.

Similarly, the Federal Reserve’s preferred measure of inflation, core PCE, continues its fall. It grew just 0.1% for the month in May and 2.6% on an annual basis, its slowest pace since late 2020.

The CME ratewatch tool now has the probability of a cut in September at 64% compared to 51% a month earlier.

China has been showing some positive signs in manufacturing and exports. May’s exports increased by 7.6% on an annual basis. The Caixin Manufacturing PMI increased to a two year high for May (see chart below). The official measure shows manufacturing still contracting in May. The Caixin measure is broader and includes smaller and more dynamic manufacturers.

However, concerns remain over potential US and EU responses to surging Chinese exports. On 12 June, the EU announced new tariffs on Chinese EVs, following the US’s announcement of tariffs in May.

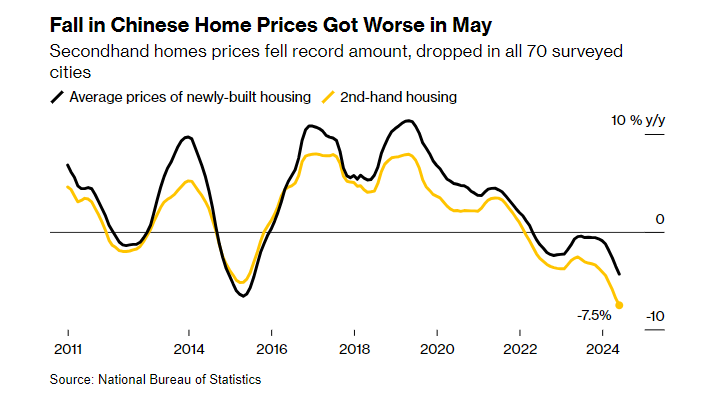

Housing remains a drag. While housing sales stabilised in May, prices continued to fall (see chart below)

After 9 months of holding, the ECB cut its interest rates by 25 bps in June. The ECB had communicated the prospect of a cut well in advance of the meeting and so it was no surprise.

However, what did surprise was the ECB slightly increasing its inflation forecasts. When asked about this, ECB president Christine Lagarde explained that despite the slight increases, the ECB is confident that inflation is still decreasing. Further, while the ECB cut rates, monetary policy remains restrictive. It is still a wait and see approach rather than the definite start of a cutting cycle. To underline this, inflation increased from 2.4% in April to 2.6% in May on an annual basis.

“We are moderating the level of restriction that applies. That’s exactly what we are doing at the moment. How long will that take? As I said, I cannot tell you now. At what speed will it happen? I cannot tell you now either. It will be delivered by the data.” Christine Lagarde.

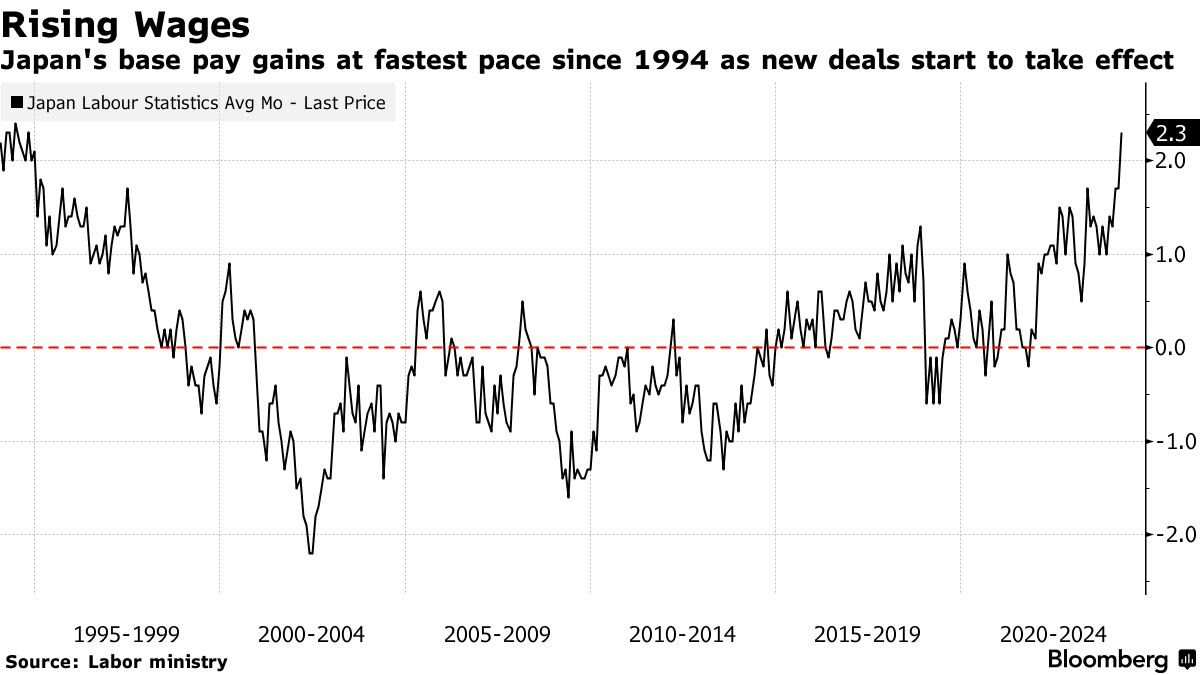

Japan’s base wages increased by 2.3% on an annual basis in April, the largest increase since 1994 (see chart below). This is good news for the Bank of Japan who is hoping that a cycle of inflation and moderate wage increases takes hold and confines Japan’s period of deflation to history.

During June, the BoJ governor signalled his confidence in the direction of the Japanese economy by announcing plans for further reductions in expansionary policies.

“It is appropriate to reduce the bond purchases in a predictable manner while also ensuring flexibility for market stability. If we are to start reducing [the purchases], we believe the size will be significant,” Kazuo Ueda, BoJ governor.

UK inflation has now decreased from 3.2% in March to 2% in May on a yearly basis. Although inflation is now at the BOE’s target, it kept rates unchanged in June citing the need to ensure that inflation can remain at the target rate over the medium term. While inflation has fallen dramatically over the last 6 months, inflationary pressures remain and the BoE wants stability.

New Zealand returned to positive growth in the March quarter ending its half-year recession (see chart below).

Australia is starting to look the odd one out with inflation proving stubborn. However, it was only last year that the UK was in the same situation. However, inflation has fallen dramatically in the UK as growth slowed. Growth needs to slow a little further in Australia. In the meantime, private debt investors can continue to enjoy high floating rates.