Central banks do Dusty Springfield

01 May 2024

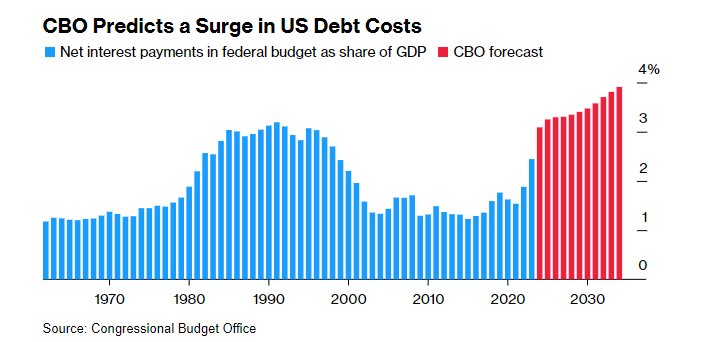

Have you ever looked at your credit card or mortgage interest payments and felt sick? Well, the US federal government is expected to pay USD 870 billion in interest payments this year which is around USD 48 billion more than it is expected to spend on defence. Worse still, its debt interest payments are expected to increase from 2.4% of GDP in 2023 to 3.9% by 2034 (see chart below).

Jamie Dimon, JPMorgan Chase CEO, recently described US debt as “a cliff that we’re going 60 mph towards.” While former quant trader and author of the “Black Swan”, Nassim Nicholas Taleb, said that the US is approaching a “debt spiral”. Even the phlegmatic Fed Chairman Jerome Powell recently admitted that, “It’s probably time, or past time, to get back to an adult conversation among elected officials about getting the federal government back on a sustainable fiscal path.”

In this edition of Chart of the month, we look at the size of the debt and ask whether the US (and by implication the rest of the world) is in trouble.

The chart below shows that US federal debt (adjusted for inflation) jumped during the Second World War but was then steady until 1983 when it was impacted by President Reagan’s personal income tax cuts and increased defence spending.

However, in the last 20 years the debt has nearly tripled in value. In particular, it accelerated during the 2008-09 Global Financial Crisis and the COVID-19 pandemic. The US government spent big on stimulus payments and also felt the impact of the automatic stabilisers (increased social spending and lower tax revenue during economic downturns). There were also its involvement in wars in the Middle East.

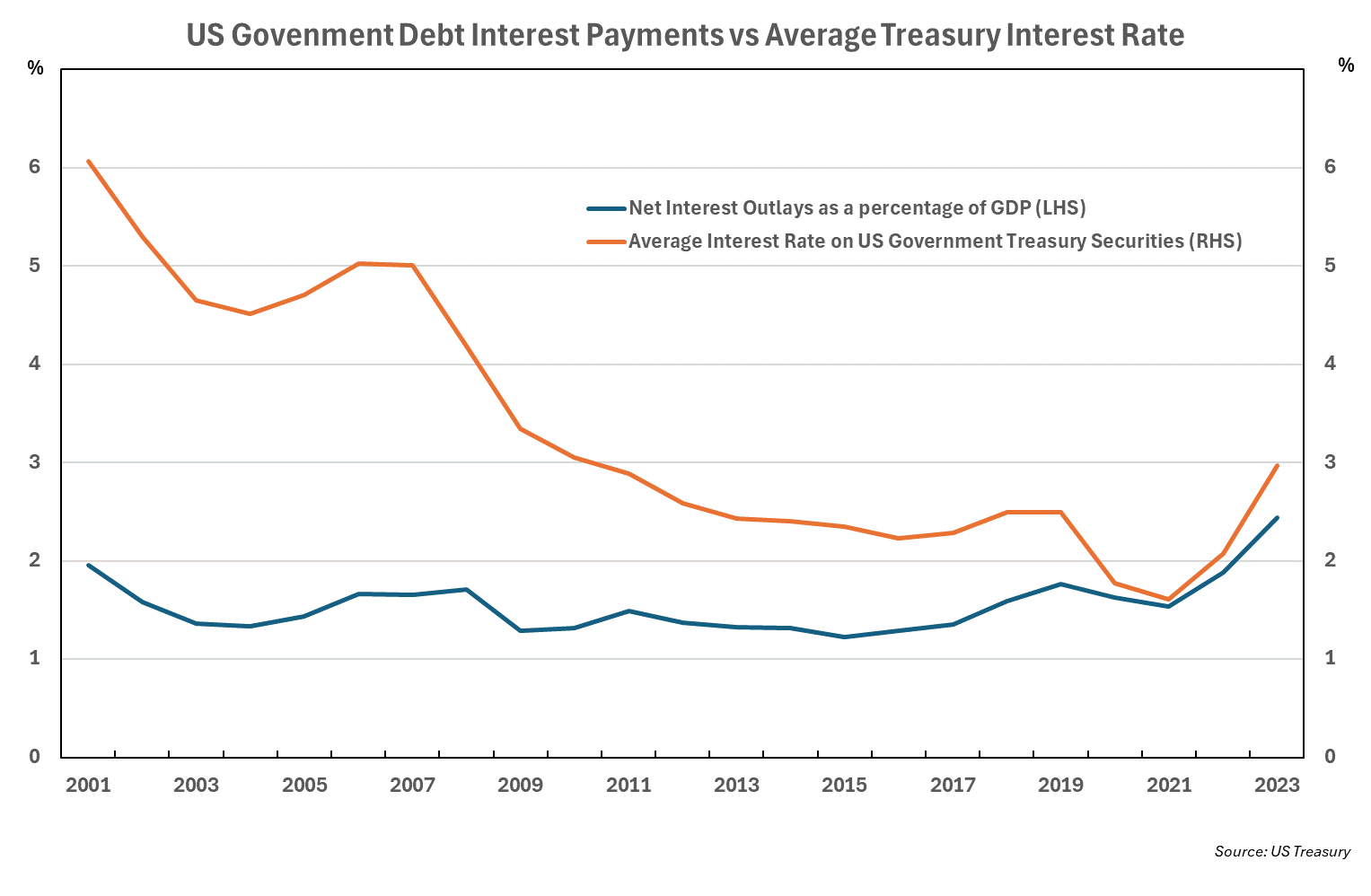

Despite the explosion in US government debt in the 2000s, interest payments as a percentage of GDP actually decreased during the 2000s (see our first chart). Why? Shouldn't the interest payments have increased as the level of debt increased? If interest rates had stayed the same, that would have been the case but the average interest rate on US Treasury securities has mostly decreased in the 2000s. It is only recently, as the average interest rate has increased (as the Fed has raised the Fed Funds rate to fight inflation) that the debt interest payments have sharply risen as a percentage of GDP (see chart below).

The short answer is when investors, particularly foreign governments, stop buying US treasuries. For a normal economy as government debt and debt interest payments climb higher, demand for the government’s debt will fall even as it offers higher yields. The national currency will then come under pressure to devalue and the country could face default, which will make it harder for it to borrow in the future. This is obviously devastating for any national economy, Argentina is a prime recent example.

However, to say that the US is no normal country is an understatement. It is the world’s largest economy and since the Bretton Woods Conference in 1944, the US dollar has been the global reserve currency. This means that there is intrinsic demand for US dollars that has little to do with what is happening to the US economy.

However, history tells us that the US dollar will not remain a global reserve currency forever. It will eventually go the way of the Byzantine solidus, the Arab dinar, the Spanish silver dollar, and the Pound sterling. Already the Chinese have been trying to move away from US dollar reserves, even as it continues to be one of the largest buyers of US treasuries (Japan is currently the largest).

Typically, the reserve currency status is lost as the underlying country declines in economic power. Increasing government debt, if left unchecked, could be one of the factors that helps erode US power.

While the regular pantomimes in the US Congress and Senate over the debt ceiling does little to inspire confidence, the day of US collapse is unlikely to be anytime soon. The US debt situation would need to get a lot worse. For example, US government debt is 123% of GDP in 2024 which although high is below the average for the G7, which includes Japan at 255%.

The interest rate on US treasuries will likely also fall over the next few years as the Fed funds rate falls. This will help lessen the debt interest payments. However, the Fed fund rate will not go all the way back to zero as was the case pre-pandemic.

If the US were to ever default on its debt, not only would it send the global economy into a deep recession but it could also lead to a new economic order: the end of Bretton Woods, its institutions, and the WTO! The transition period to a new steady state would likely be tumultuous if history is the judge.

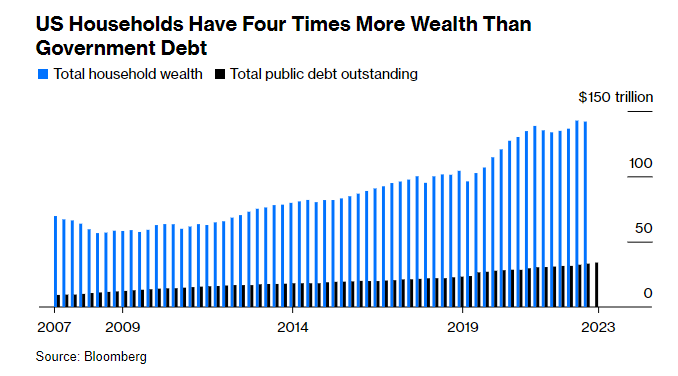

However, not all economists are worried. Economists like Claudia Sahm and Stephanie Kelton point to the size of US wealth compared to US government debt (see chart below). They argue that if push comes to shove, the US government will just increase taxes to increase government revenue.

Of course that will not be popular, as evidenced by their reluctance to raise taxes in the last few years despite the need. In fact recent administrations have cut taxes! However, at some point a US President, Congress, and the Senate will have a “come to Jesus” moment and taxes will be raised - like they were in the 1990s, which was the last time debt interest payments got out of hand (see the first chart again).

Increasing US government debt and debt interest payments means very little in the short and medium term for Australian Private Debt. At the margins, it may increase the relative attractiveness of the Australian market. If the US were to ever have a true debt crisis then Australia would not have time to think about the repercussions for its private debt market - it would be like winning a raffle on the Titanic.