The RBA does not want to have to raise rate but it is deeply concerned about the forecasted path of inflation. Inflation is now expected to take even longer to fall within the target band! For the moment, the Board deems rates are restrictive enough, just. However, we are just one or two data points away from a rise. And don’t expect a rate cut (or two) for Christmas.

The RBA did not raise rates as early nor as high as other central banks as it believed that was the best way to navigate the narrow path between reducing inflation and preserving low unemployment in the Australian context. However, the Australian economy is proving more robust than its peers. So Australia's narrow path will remain restrictive, for now, even as interest rates begin to fall elsewhere.

What the RBA’s Statement said

“In year-ended terms, underlying inflation has now been above the midpoint of the target for 11 consecutive quarters. And quarterly underlying CPI inflation has fallen very little over the past year.”

“The central forecasts set out in the latest SMP are for inflation to return to the target range of 2–3 per cent late in 2025 and approach the midpoint in 2026. This represents a slightly slower return to target than forecast in May, based on estimates that the gap between aggregate demand and supply in the economy is larger than previously thought. In part, this reflects an increase in the forecast for domestic demand. But it also reflects a judgement that the economy’s capacity to meet that demand is somewhat weaker than previously thought, evidenced by the persistence of inflation …”

“... momentum in economic activity has been weak, as evidenced by slow growth in GDP, a rise in the unemployment rate and reports that many businesses are under pressure.”

“Policy will need to be sufficiently restrictive until the Board is confident that inflation is moving sustainably towards the target range.”

Statement by the Reserve Bank Board: Monetary Policy Decision, 6 August 2024.

“For now the Board judges that the level of the cash rate is appropriate for balancing our inflation and employment objectives but there are still some considerable uncertainties. And I want to highlight here that there is still a risk that inflation will take too long to return to target.”

“Demand has been above supply for some time now and that is why inflation has been so persistent.”

“While growth of demand has been slow, there’s actually no guarantee that supply and demand will return to balance quickly enough.”

“A rate cut is not on the agenda in the near term.”

“If the Board feels that in the next 6 to 12 months that we’re not even tracking to get back into the top of the band by the end of 2025, then I think there will be some very difficult decisions to make.”

“Are we heading for recession? I don’t believe so and the Board doesn’t believe so because we still believe that we are on that narrow path.”

“We would really like productivity to get back to its trend levels from prior to the pandemic after it all got thrown out and that’s going to be really key to the fortunes of the country.”

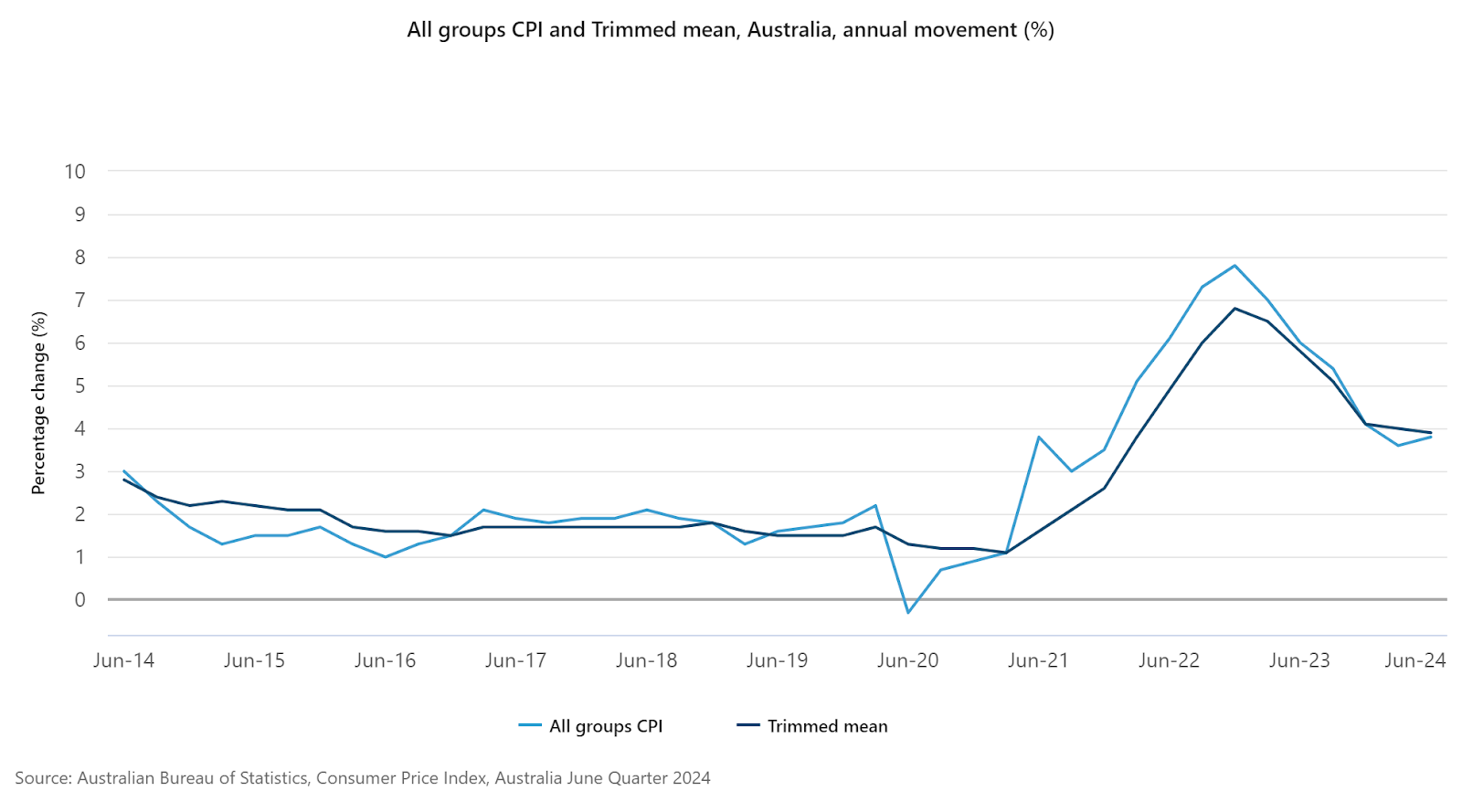

No jump scare from June-quarter CPI

All eyes were fixed on the release of the June-quarter CPI on 31 July. Some commentators tipped inflation to be higher than expected and that this would force the RBA to raise rates. Bullock breathed a sigh of relief; inflation was higher but came in at the expected 3.8%. While the RBA’s preferred measure, the trimmed mean, actually fell from 4% to 3.9% (see chart below). The RBA did not have to increase rates and could keep them at the current restrictive levels.

Increased aggregate demand will keep inflation higher for longer

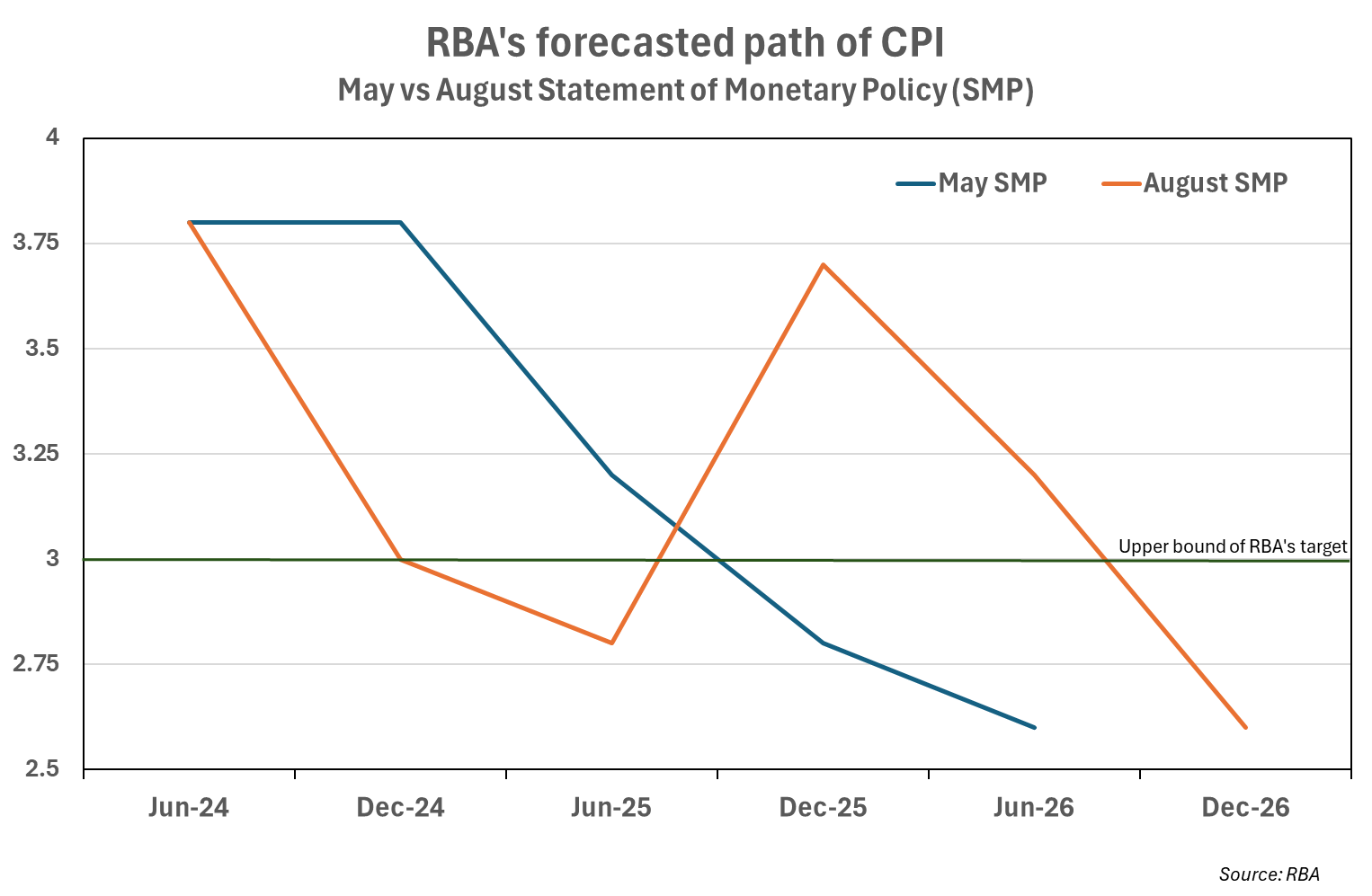

While the June CPI did not surprise, the RBA’s Statement on Monetary Policy (SMP) for August has surprised. The forecast for 2024 public sector demand has increased from 1.5% year-ending in the May SMP to 4.3% in the August SMP. This is a result of increased government spending announced in the federal and state budgets. The forecast for household consumption has increased from 1.3% in May to 1.5% in August.

Final demand in the first-half of 2024 was also higher than the RBA expected.

While consumers are under pressure, the economy isn’t slowing as much as the RBA wants.

As a result of this higher than expected demand, real and forecasted, the RBA now expects that headline inflation will not fall within its target band of 2% to 3% until much later than previously thought: December 2026 versus December 2025 (see chart below).

Inflation will actually temporarily dip into the middle of the ban in the middle of 2025 because of the federal government’s extended electricity rebates and increase in rent assistance before the unwinding of policies sees it move above the band in late 2025.

This stretching out of the time horizon for high inflation deeply concerns the bank as it does not want to see high inflation expectations become entrenched in the economy.

If inflation does take until late 2026 to fall within the target band, that will mark 5 years since it first jumped above the band in December 2021. The RBA would love to see this period shorten and will definitely work to ensure that it is not any longer than 5 years.

The RBA’s bargain

Looking back, the RBA has chosen to err on the side of employment and growth more so than its peers. So while Australia did not have a recession like the UK, New Zealand, and some parts of Europe, it is now paying the price of higher-for-longer interest rates. This is the narrow path the RBA has chosen. The RBA has eschewed short-term pain for a longer period of lesser pain.

If upward risks to inflation come to bear over the next 12-months in Australia, criticisms of the RBA’s conservative approach will grow louder. But If inflation starts to grow again overseas, then the criticism will subside. Either way, rates aren’t coming down before Christmas.

Impact on the Australian Private Debt Market

With interest rates expected to be higher for longer in Australia and the economy appears to be more resilient than previously expected, Australia remains a very attractive option for private debt investors.